Monthly Market Summary

Market Leadership Continues to Broaden Amid Questions About AI’s Impact

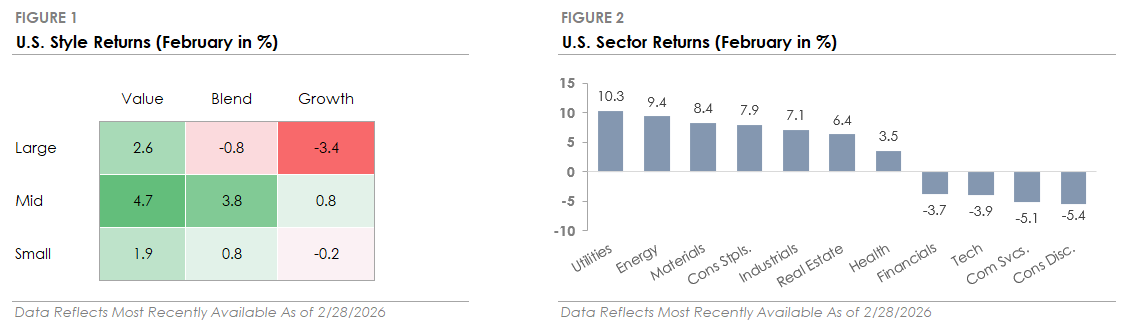

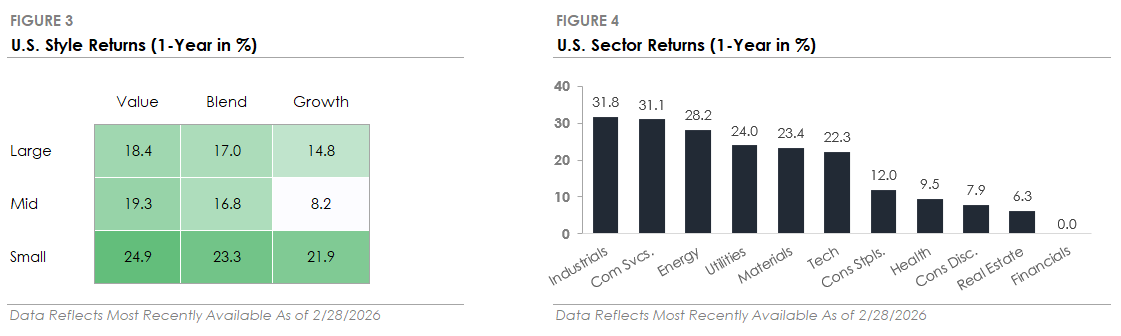

The rotation away from mega-cap tech stocks that started in January extended into February. While the S&P 500 traded lower, the average stock, as measured by the equal-weighted index, gained over +3%. The rotation was broad-based: small caps outperformed large caps, value beat growth, seven of eleven sectors beat the S&P 500, and international stocks outpaced U.S. stocks. Market leadership is broadening after a long period in which a small group of mega-cap tech stocks drove most of the market’s gains, and diversified portfolios are benefiting from the rotation.

The technology sector’s weakness was tied to concerns that artificial intelligence will impact, and potentially disrupt, current business models. A wave of AI product launches caused investors to rethink not only the potential winners, but also which industries could face disruption, such as software, consulting, real estate services, freight brokers, and other industries where AI capabilities are advancing rapidly. The selling and volatility were most pronounced early in the month but later stabilized as the narrative shifted toward a more balanced view of AI as a tool that enhances existing businesses rather than replaces them. The disruption fears eased into month-end, but investors are likely to remain focused on AI's impact on industries beyond technology.

Bonds & Gold Trade Higher as Investors Seek Stability

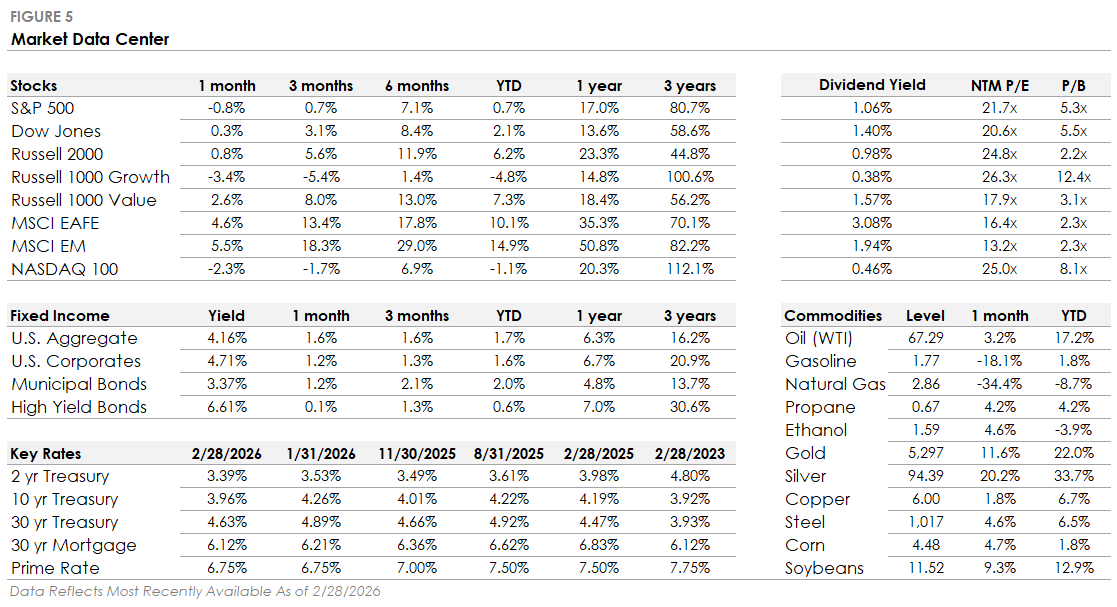

February was a strong month for bonds, as the 10-year Treasury yield fell nearly -0.30% to end the month below 4.00%, the lowest since October. The decline in Treasury yields drove the bond market rally, with longer-maturity and higher-quality bonds outperforming as investors sought stability amid tech sector volatility, trade policy uncertainty tied to the Supreme Court’s tariff ruling, and rising geopolitical tensions with Iran. Long-duration Treasuries gained +4.1%, and mortgage-backed securities returned +1.6%, both outperforming the broad U.S. Bond Aggregate Index.

The bond rally is notable because it occurred even as expectations for interest rate cuts were pushed further out. The Federal Reserve held interest rates steady at its January meeting after cutting in December, and the market doesn’t expect the next rate cut until June, at the earliest. The distinction is important: falling Treasury yields reflected investor demand for lower volatility assets amid the tech sector sell-off and geopolitical tensions, not a signal that economic conditions are deteriorating. Gold gained more than +10% in February, reflecting the same demand for portfolio protection.

Minutes from the Fed's January meeting signaled a continued focus on controlling inflation, and the economic data supports the Fed's patience. The labor market added +130,000 jobs in January, the unemployment rate declined to 4.3%, and an index of manufacturing activity crossed back into expansion for the first time in nearly a year. Inflation continues to ease, with core CPI rising at a +2.5% annual rate, the slowest since early 2021. The combination of steady growth and cooling inflation gives the Fed room to remain on hold. While the market still expects the Fed to cut twice this year, the start date keeps drifting later.

Where Markets Stand Today

February was a busy month filled with AI headlines, shifting market leadership, and policy uncertainty. But beneath the surface, the economic backdrop remains stable, and the Federal Reserve remains patient. As leadership broadens beyond a narrow group of mega-cap stocks, diversified portfolios are beginning to benefit from a healthier market structure.

Important Disclosures

Views expressed are as of the date indicated, based on the information available at that time, and may change based on market or other conditions. Investment decisions should be based on an individual’s own goals, time horizon, and tolerance for risk. Investing involves risk, including risk of loss. Investment advisory services provided by Provident Financial Planning, LLC, a SEC-Registered Investment Advisor.

The information and opinions provided herein are provided as general market commentary only and are subject to change at any time without notice. This commentary may contain forward-looking statements that are subject to various risks and uncertainties. None of the events or outcomes mentioned here may come to pass, and actual results may differ materially from those expressed or implied in these statements.

No mention of a particular security, index, or other instrument in this report constitutes a recommendation to buy, sell, or hold that or any other security, nor does it constitute an opinion on the suitability of any security or index. The report is strictly an informational publication and has been prepared without regard to the particular investments and circumstances of the recipient.

Past performance does not guarantee or indicate future results. Any index performance mentioned is for illustrative purposes only and does not reflect any management fees, transaction costs, or expenses. Indexes are unmanaged, and one cannot invest directly in an index. Index performance does not represent the actual performance that would be achieved by investing in a fund.

Subscribe to receive the latest blog posts to your inbox every week.

Explore our expertly curated articles offering deeper knowledge and understanding on a range of financial topics.

Guided by our values of faith, service, and transparency, we at Provident Financial Planning are ready to help you navigate your financial journey. Schedule a consultation with us and discover how we can create a personalized financial plan for you.