On July 4, 2025, Donald J. Trump passed the One Big Beautiful Bill Act (OBBBA), marking one of the most substantial tax and fiscal reforms in recent U.S. history. The bill builds upon key pillars of the 2017Tax Cuts and Jobs Act (TCJA) while introducing sweeping changes to deductions, small business taxation, charitable giving, estate planning, and entitlement funding. While its name may evoke a sense of grandeur, the bill’s true power lies in the intricate details and planning strategies it enables—or in some cases, demands. For wealth managers, understanding the depth and breadth of these provisions is not just prudent—it’s essential.

Tax Strategy: Tactical Adjustments in a Shifting Landscape

The OBBBA fundamentally reshapes the tax planning landscape with both expansions and limitations. For high-income earners and small business owners, the permanent 20% Qualified Business Income (QBI) deduction for pass-through entities eliminates the previous sunset risk and allows for more confident long-term business planning. Tax strategists can now build multi-year income stacking or distribution plans with more clarity around net taxable income.

In addition, the overhaul of the Qualified Small Business Stock (QSBS) rules introduces tiered capital gain exclusions: 50% after three years, 75% after four years, and 100% after five years. This revision not only encourages earlier liquidity events but also makes it more tax-efficient to hold and exit early-stage business investments. Strategic harvesting of QSBS gains becomes essential, especially when paired with gain deferral tools or gifting strategies.

Wealth managers must also remain vigilant of the bill’s changes to charitable deductions. While the return of an above-the-line charitable deduction—$1,000 for individuals and $2,000 for married couples—provides relief for non-itemizers, wealthier clients face new limits. Itemized charitable deductions are now capped at 35% of AGI, with a 0.5% AGI floor required to qualify. This places renewed emphasis on Donor-Advised Funds (DAFs), charitable bunching, and qualified charitable distributions (QCDs) for optimizing philanthropic plans in high-income years.

From a timing perspective, the bill offers incentives to accelerate income or capital gains into the current legislative environment. With growing concern over long-term deficits—the bill is projected to increase the national debt by $3trillion—many strategists foresee future tax increases, particularly for high-net-worth households. Locking in current rates through Roth conversions, trust funding, or harvesting embedded gains may be prudent.

Financial Planning: New Rules, New Opportunities

The OBBBA introduces a series of targeted deductions and incentives aimed at wage earners, seniors, and families. At the center of these changes is the permanent extension of the Tax Cuts and Jobs Act’s (TCJA) standard deduction, which has now increased to $15,750 for individuals and $31,500 for joint filers. This simplifies returns and reduces the tax burden for many Americans, especially those who do not itemize.

The bill also introduces above-the-line deductions for income types that were previously taxable. Service industry workers can now deduct up to $25,000 in tip income, while employees working overtime may claim up to $12,500 annually. These deductions lower adjusted gross income (AGI), which not only reduces federal tax liability but can also help clients qualify for income-based benefits such as education credits, Affordable Care Act subsidies, and Roth IRA eligibility.

Planners will also want to take note of the $10,000 interest deduction for U.S.-assembled vehicle loans and a new $6,000 senior deduction for taxpayers aged 65 or older. These changes expand the universe of tax-sheltered expenses and demand revised budgeting, especially for retirees on fixed incomes.

Moreover, the introduction of “Trump Accounts”—a new, flexible, tax-deferred savings vehicle—presents a fresh tool for planners. With government-seeded $1,000 and $5,000 annual contribution limits, these accounts can be used for education, first-time home purchases, or disability-related costs. Their flexibility positions them as potential complements or alternatives to 529 plans or Roth IRAs, particularly for younger clients or lower-income households.

Wealth Management: Positioning Portfolios and Business for the Long Term

For wealth managers, the OBBBA opens up new possibilities in portfolio construction, business succession planning, and risk mitigation. The QSBS enhancements, combined with expanded Section179 expense limits ($2.5 million), create strong incentives to grow and scale small businesses with an eye toward eventual liquidity events. Managers serving entrepreneurs or family offices should review cap tables, investment timelines, and shareholder agreements to align with the new holding period incentives.

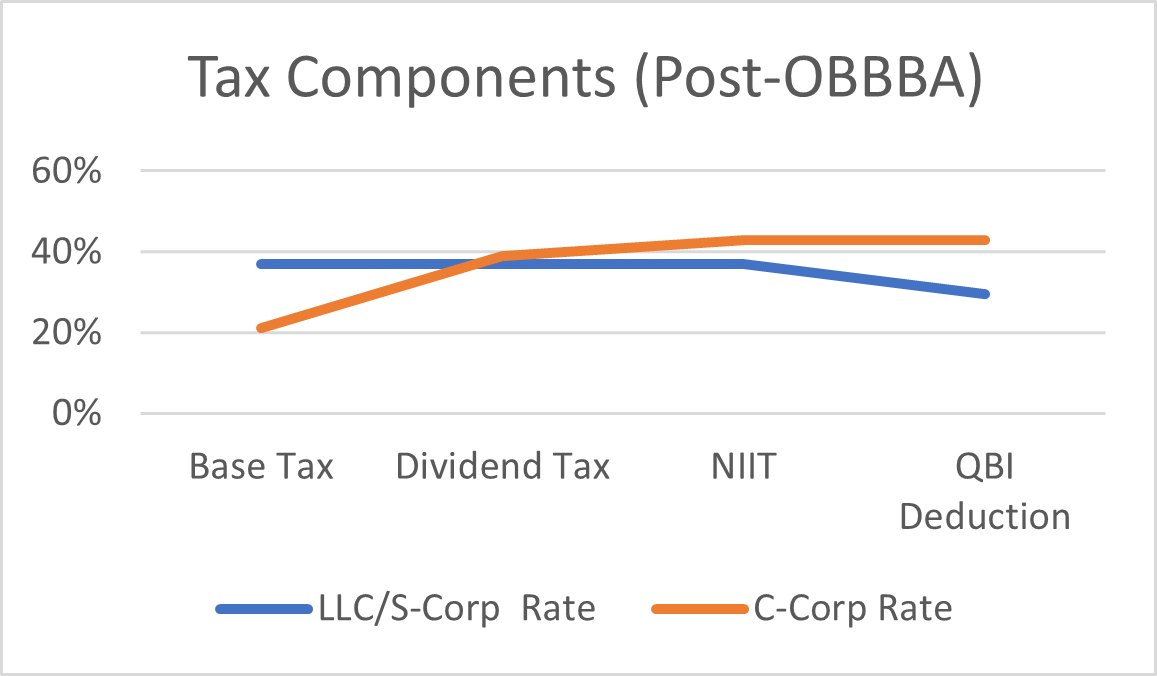

Additionally, the permanent expansion of the QBI deduction changes how pass-through businessowners weigh their entity structures. It may now be advantageous to remain as an S-Corp or LLC rather than converting to a C-Corp, especially considering ongoing double-taxation risks. For example, pass-through entities enjoy the QBI deduction effectively lowering the top marginal federal tax rate from 37% to 29.6%. C-Corps pay 21% corporate income tax on profits, and when those profits are distributed as dividends, shareholders are taxed again- typically at a qualified dividend rate of 15-20%, plus the 3.8% Net Investment Income Tax (NIIT) for high earners. This leads to a combined tax rate of 39.8%-44.6% on distributed earnings. By contrast, an S-Corp or LLC is only taxed once on their share or business income while C-Corps face double taxation.

On the public market side, managing client exposure to potential tax increases means reevaluating asset location strategies. Allocating high-yield or high-turnover assets into tax-deferred or exempt accounts while reserving low-turnover equities or municipal bonds for taxable accounts remains sound practice—but must now account for new AGI thresholds and the potential for charitable limitations.

Estate Planning: A Historic Gifting Opportunity

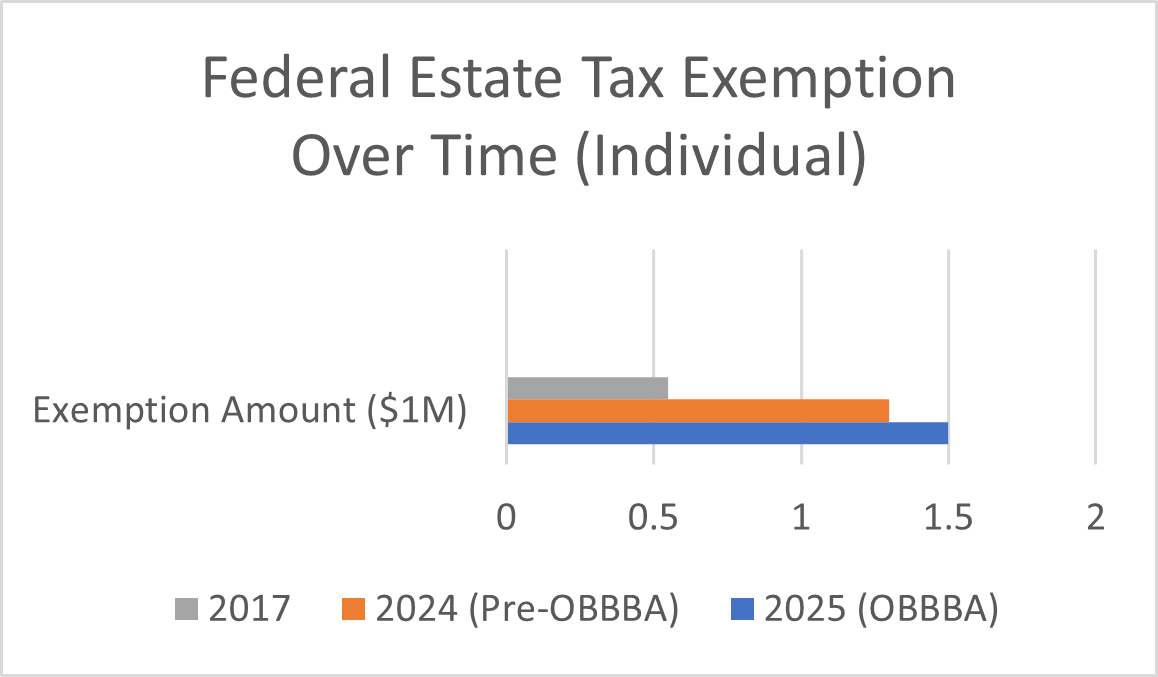

Perhaps the most dramatic opportunity presented by the OBBBA is the doubling of the federal estate and gift tax exemption. The exemption now stands at $15 million per individual and $30 million per married couple, creating an unprecedented window for intergenerational wealth transfer.

This provision alone should prompt immediate review of estate plans, particularly for high-net-worth clients who were previously constrained by lower thresholds.

Families can use this expanded exemption to fund dynasty trusts, execute large-scale lifetime gifts, or restructure grantor trusts without triggering transfer tax. Coupled with the relatively low-interest rate environment, GRATs and SLATs become even more effective at leveraging appreciation outside the estate.

However, this window maybe fleeting. The legislation’s cost and political volatility suggest that a future administration could roll back the exemption to pre-2018 levels or lower. Clients should act with urgency to “lock in” today’s higher exemption while considering valuation discounts, closely held business interests, and planned liquidity events.

Moreover, with charitable limitations now codified into tax law, estate strategies involving charitable remainder trusts (CRTs) or private foundations may require reengineering. Advisors must work closely with legal counsel to ensure these structures remain compliant and efficient under the new AGI rules and deduction caps.

Firm Disclosures

Views expressed are as of the date indicated, based on the information available at that time, and may change based on market or other conditions. Investment decisions should be based on an individual’s own goals, time horizon, and tolerance for risk. Investing involves risk, including risk of loss. Investment advisory services provided by Provident Financial Planning, LLC, a SEC-Registered Investment Advisor.

The information and opinions provided herein are provided as general market commentary only and are subject to change at any time without notice. This commentary may contain forward-looking statements that are subject to various risks and uncertainties. None of the events or outcomes mentioned here may come to pass, and actual results may differ materially from those expressed or implied in these statements. No mention of a particular security, index, or other instrument in this report constitutes a recommendation to buy, sell, or hold that or any other security, nor does it constitute an opinion on the suitability of any security or index. The report is strictly an informational publication and has been prepared without regard to the particular investments and circumstances of the recipient.

Past performance does not guarantee or indicate future results. Any index performance mentioned is for illustrative purposes only and does not reflect any management fees, transaction costs, or expenses. Indexes are unmanaged, and one cannot invest directly in an index. Index performance does not represent the actual performance that would be achieved by investing in a fund.

Subscribe to receive the latest blog posts to your inbox every week.

Explore our expertly curated articles offering deeper knowledge and understanding on a range of financial topics.

Guided by our values of faith, service, and transparency, we at Provident Financial Planning are ready to help you navigate your financial journey. Schedule a consultation with us and discover how we can create a personalized financial plan for you.