Many people spend their careers focused on reaching the next salary milestone or securing a promotion, but financial progress shouldn't be measured by your paycheck alone. The decisions you make in your peak earning years are just as important as the size of your paycheck. One of the most significant risks is lifestyle creep, which is the tendency for everyday spending to rise alongside income. How you manage a salary raise today can have a significant impact on your long-term financial security. Without a strategy for handling salary increases, even a high-earning household can find themselves ill-prepared for the future.

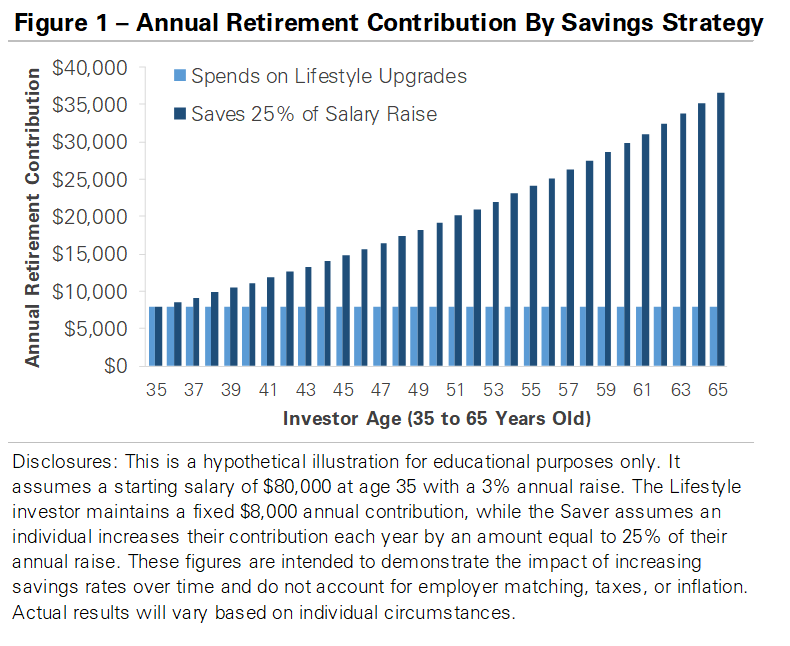

The charts below demonstrate how different approaches to a salary increase can impact a retirement portfolio’s growth. They’re based on a hypothetical scenario: two individuals aged 35 make $80,000 annually and receive 3% annual raises. Both start by contributing 10% of their salary, or $8,000, to retirement savings. The two sets of bars in Figure 1 track different strategies for managing the raises and retirement contributions. The Lifestyle individual keeps their annual contribution fixed at $8,000. Every dollar of every raise is spent on immediate lifestyle upgrades, such as a nicer car, another trip, or higher discretionary spending. The Saver individual takes a more balanced approach, setting aside 25% of every raise while enjoying the rest. For example, a $2,000 raise would increase the next year’s contribution by $500, or 25%.

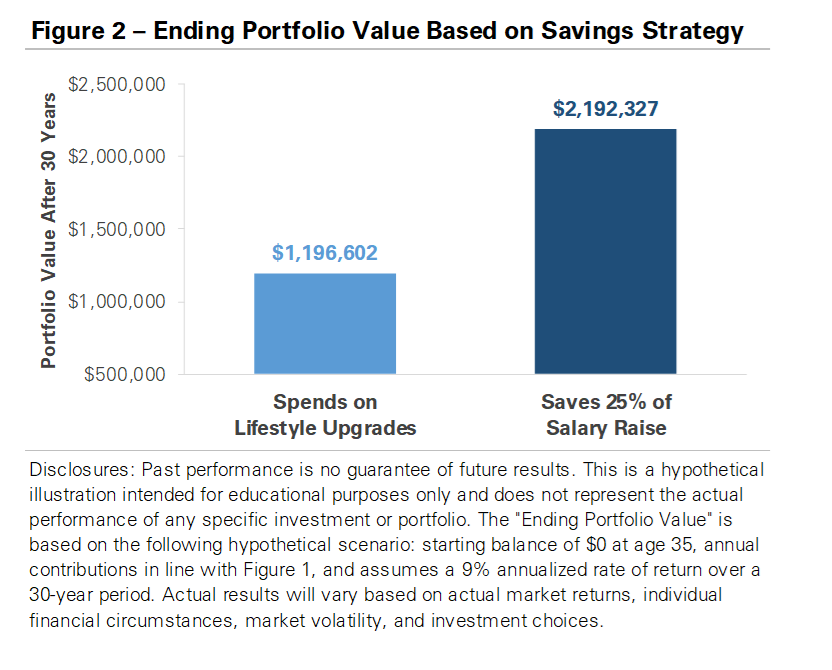

While both individuals earn the same amount, their retirement savings quickly diverge. Figure 2 graphs the ending portfolio values at age 65, reflecting 30 years of each individual’s savings strategy. These hypothetical ending account values assume the portfolios earn a +9% annual return. Over 30 years, the Lifestyle individual contributed nearly $250,000, which grew to nearly $1.2 million. The Saver individual contributed nearly $630,000, which grew to nearly $2.2 million, almost $1,00,000 larger than their peer’s. The difference isn’t just additional savings but decades of compounding that can extend a portfolio’s life in retirement or create the option to retire earlier. In contrast, the Lifestyle individual not only saves less but also increases their base cost of living, which will require a larger portfolio to sustain their lifestyle in retirement.

Building long-term wealth isn’t just about what you earn; it’s about how you manage the surplus as you earn it. Raises can either disappear into lifestyle upgrades or become a powerful tool for future security and flexibility. It’s about finding a balance between enjoying the reward of hard work today and saving for your future. There’s no one-size-fits-all approach, and the method you start with doesn’t have to be permanent. Everyone’s retirement looks different, and the right strategy depends on your goals and life stage. Our goal is to help you create a savings strategy tailored to your unique needs and goals so that when the time comes, you’re ready to enjoy retirement.

Important Disclosures

Views expressed are as of the date indicated, based on the information available at that time, and may change based on market or other conditions. Investment decisions should be based on an individual’s own goals, time horizon, and tolerance for risk. Investing involves risk, including risk of loss. Investment advisory services provided by Provident Financial Planning, LLC, a SEC-Registered Investment Advisor.

The information and opinions provided herein are provided as general market commentary only and are subject to change at any time without notice. This commentary may contain forward-looking statements that are subject to various risks and uncertainties. None of the events or outcomes mentioned here may come to pass, and actual results may differ materially from those expressed or implied in these statements. No mention of a particular security, index, or other instrument in this report constitutes a recommendation to buy, sell, or hold that or any other security, nor does it constitute an opinion on the suitability of any security or index. The report is strictly an informational publication and has been prepared without regard to the particular investments and circumstances of the recipient.

Past performance does not guarantee or indicate future results. Any index performance mentioned is for illustrative purposes only and does not reflect any management fees, transaction costs, or expenses. Indexes are unmanaged, and one cannot invest directly in an index. Index performance does not represent the actual performance that would be achieved by investing in a fund.

Subscribe to receive the latest blog posts to your inbox every week.

Explore our expertly curated articles offering deeper knowledge and understanding on a range of financial topics.

Guided by our values of faith, service, and transparency, we at Provident Financial Planning are ready to help you navigate your financial journey. Schedule a consultation with us and discover how we can create a personalized financial plan for you.